SPVs

SPV vs Fund Structure: Choosing the Right Investment Vehicle in Private Markets

SPV vs Fund Structure: Choosing the Right Investment Vehicle in Private Markets

Addhyan Negi

·

As private markets mature and investor sophistication increases, the question of SPV vs fund structure has become central to how capital is deployed. Venture capital firms, private equity managers, family offices, and even individual accredited investors are no longer limited to traditional blind-pool funds. Instead, they are increasingly evaluating deal-by-deal structures such as Special Purpose Vehicles (SPVs) alongside conventional fund models.

While both SPVs and funds are designed to pool capital and allocate it into private investments, they differ significantly in structure, economics, governance, flexibility, and investor experience. Choosing between an SPV and a fund structure is not merely a legal decision—it directly affects risk exposure, liquidity, transparency, and long-term capital efficiency.

Understanding the SPV Structure

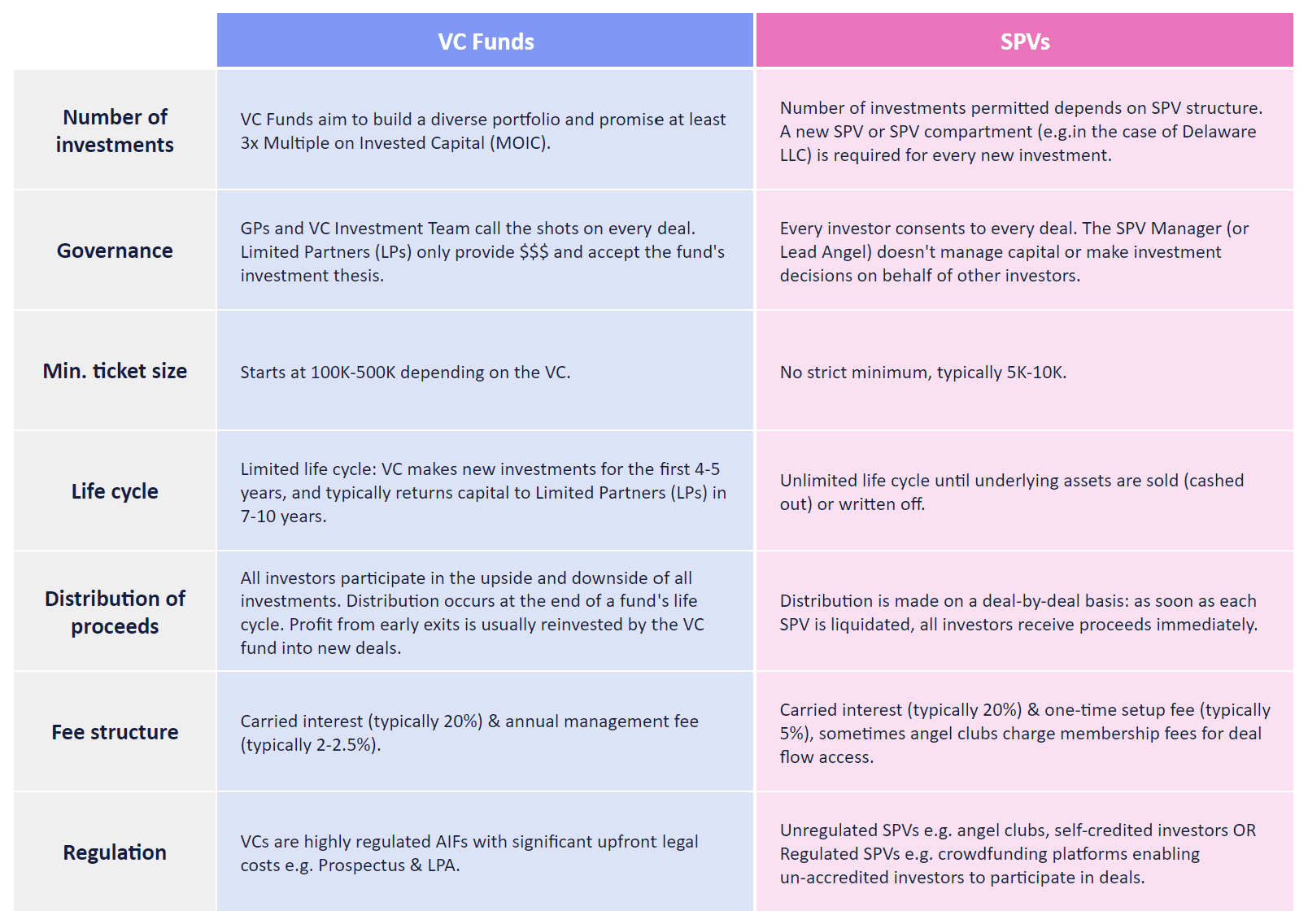

A Special Purpose Vehicle (SPV) is a standalone legal entity created for a single, clearly defined investment purpose. The SPV typically holds one asset, one deal, or exposure to a specific transaction. Investors do not invest directly into the underlying company or asset; instead, they invest into the SPV, which owns that exposure.

The defining feature of an SPV is ring-fencing. Assets, liabilities, cash flows, and risks associated with the investment are isolated within the SPV. If the investment underperforms or fails, losses are limited to the capital committed to that SPV, without affecting other investments held by the same sponsor or investor.

SPVs are commonly structured as LLCs or limited partnerships and are widely used in venture capital syndicates, private equity co-investments, real estate acquisitions, and structured credit transactions.

Understanding the Fund Structure

A fund structure, by contrast, is a multi-asset investment vehicle designed to deploy capital across several investments over a defined investment period. Investors commit capital upfront, often for a long duration, and grant the fund manager discretion to allocate that capital according to the fund’s strategy.

Traditional funds operate as blind pools. While the investment mandate is clearly defined, investors typically do not have approval rights over individual deals. Instead, they rely on the fund manager’s expertise, track record, and governance framework.

Funds are usually structured as limited partnerships, with a general partner (GP) managing the fund and limited partners (LPs) providing capital. This model dominates institutional investing due to its scalability and diversification benefits.

Capital Deployment: Deal-Specific vs Pooled Strategy

One of the most important distinctions in the SPV vs fund structure debate is how capital is deployed.

In an SPV structure, capital is deployed deal by deal. Investors evaluate a specific opportunity, assess its risk-return profile, and commit capital only if it aligns with their objectives. This creates a high degree of intentionality and precision in portfolio construction.

In a fund structure, capital is pooled and deployed over time across multiple deals. While this provides diversification, it reduces investor control. Capital may be allocated to investments that individual LPs would not have chosen independently.

This difference makes SPVs particularly attractive for co-investments, thematic exposure, and opportunistic strategies, while funds remain well-suited for broad mandates and long-term capital deployment.

Transparency and Investor Control

Transparency is a major factor driving the growing adoption of SPV structures.

SPVs offer full deal-level transparency. Investors know exactly which asset they own, at what valuation capital was deployed, and how performance is evolving. Reporting is typically simpler and more focused, as it relates to a single investment.

Fund structures, while professionally managed, provide aggregated transparency. Investors receive portfolio-level reporting rather than granular insight into each decision. This is acceptable—and often preferred—by institutional investors seeking manager-driven diversification, but it can feel opaque to investors who want more visibility.

From a control perspective, SPVs allow investors to opt in or out of each opportunity. Funds require a higher level of trust and long-term commitment to the manager’s judgment.

Risk Profile and Diversification

Risk exposure differs significantly between SPVs and funds.

An SPV concentrates risk in a single asset or transaction. While this allows for targeted exposure and potentially higher returns, it also increases idiosyncratic risk. Poor performance cannot be offset by other assets within the same vehicle.

Funds, on the other hand, are inherently diversified. Losses in one investment may be balanced by gains in others. This diversification reduces volatility and downside risk but may also dilute upside from top-performing assets.

As a result, SPVs are often used by investors who already have diversified portfolios and are seeking incremental or opportunistic exposure, while funds appeal to those prioritizing risk smoothing and long-term allocation.

Fee Structures and Economics

The economic models of SPVs and funds differ in ways that materially impact investor returns.

Funds typically charge management fees (often around 2%) and carried interest (commonly 20%) on profits. These fees compensate managers for sourcing, executing, and managing investments over long periods.

SPVs generally have lower ongoing fees. There is usually no annual management fee, though sponsors may charge setup fees, administrative costs, and carried interest on profits. Because SPVs are deal-specific, fee structures are often more flexible and negotiable.

For investors, this means SPVs can be more cost-efficient for high-conviction opportunities, while funds justify their fees through diversification, infrastructure, and long-term stewardship.

Governance and Decision-Making

Governance frameworks also differ meaningfully between SPVs and funds.

In an SPV, governance is intentionally lightweight. A manager or sponsor executes the investment, while investors retain limited rights over major decisions such as amendments, early liquidation, or material changes to the deal.

Funds have more formal governance structures, including advisory committees, reporting standards, and regulatory oversight. This added complexity supports scale but reduces agility.

The simpler governance of SPVs makes them faster to execute and easier to customize, whereas funds prioritize stability, repeatability, and institutional standards.

Liquidity and Time Horizon

Liquidity is another key differentiator.

SPVs are generally illiquid until a defined exit event occurs. There is no expectation of interim liquidity, and secondary transfers may be restricted. Investors must be comfortable with holding the position until realization.

Funds also involve long lock-up periods, but they may generate interim liquidity through distributions from partial exits or cash-flowing assets. Additionally, institutional secondary markets for fund interests are more mature than those for SPVs.

Time horizon alignment is therefore critical. SPVs are best suited for investors with clear expectations around exit timing, while funds support longer, more flexible investment cycles.

Operational Complexity and Scalability

From an operational standpoint, funds are designed for scale. Once established, a fund can deploy capital across many deals without creating new legal entities each time.

SPVs, by contrast, require entity-level setup and administration for each deal. This includes legal formation, accounting, tax filings, and investor reporting. Historically, this limited SPVs to smaller or bespoke transactions.

However, modern fund administration and SPV platforms are rapidly reducing this friction, making SPVs scalable and repeatable without sacrificing efficiency.

When to Choose an SPV Structure

SPVs are particularly well-suited for:

Co-investments alongside lead funds

Venture capital syndicates

Real estate single-asset deals

Opportunistic or thematic strategies

Investors seeking maximum transparency and control

They are ideal when conviction is high and investors want targeted exposure without committing to a broader fund mandate.

When a Fund Structure Makes More Sense

Fund structures remain optimal for:

Broad diversification across assets

Long-term capital deployment

Institutional investors with large allocations

Strategies requiring continuous reinvestment

Manager-led portfolio construction

Funds excel when scale, diversification, and professional management outweigh the need for deal-level control.

SPV vs Fund Structure: A Strategic Choice

The debate between SPV vs fund structure is not about which is better in absolute terms. It is about strategic fit.

SPVs offer precision, transparency, and flexibility. Funds offer diversification, scale, and operational maturity. In practice, many sophisticated investors use both, allocating core capital to funds while deploying opportunistic capital through SPVs.

As private markets continue to evolve, hybrid approaches—where funds and SPVs coexist within the same investment ecosystem—are becoming increasingly common.

Final Thoughts

Understanding the differences between SPV and fund structures is essential for navigating modern private investing. Each structure serves a distinct purpose, and choosing the right one can significantly impact outcomes.

For investors, the key lies in aligning structure with objectives: risk tolerance, liquidity needs, conviction level, and desired control. For sponsors and managers, the challenge is offering the right vehicle for the right opportunity.

In today’s capital markets, flexibility is power—and mastering both SPV and fund structures is a competitive advantage.

If you want next, I can:

As private markets mature and investor sophistication increases, the question of SPV vs fund structure has become central to how capital is deployed. Venture capital firms, private equity managers, family offices, and even individual accredited investors are no longer limited to traditional blind-pool funds. Instead, they are increasingly evaluating deal-by-deal structures such as Special Purpose Vehicles (SPVs) alongside conventional fund models.

While both SPVs and funds are designed to pool capital and allocate it into private investments, they differ significantly in structure, economics, governance, flexibility, and investor experience. Choosing between an SPV and a fund structure is not merely a legal decision—it directly affects risk exposure, liquidity, transparency, and long-term capital efficiency.

Understanding the SPV Structure

A Special Purpose Vehicle (SPV) is a standalone legal entity created for a single, clearly defined investment purpose. The SPV typically holds one asset, one deal, or exposure to a specific transaction. Investors do not invest directly into the underlying company or asset; instead, they invest into the SPV, which owns that exposure.

The defining feature of an SPV is ring-fencing. Assets, liabilities, cash flows, and risks associated with the investment are isolated within the SPV. If the investment underperforms or fails, losses are limited to the capital committed to that SPV, without affecting other investments held by the same sponsor or investor.

SPVs are commonly structured as LLCs or limited partnerships and are widely used in venture capital syndicates, private equity co-investments, real estate acquisitions, and structured credit transactions.

Understanding the Fund Structure

A fund structure, by contrast, is a multi-asset investment vehicle designed to deploy capital across several investments over a defined investment period. Investors commit capital upfront, often for a long duration, and grant the fund manager discretion to allocate that capital according to the fund’s strategy.

Traditional funds operate as blind pools. While the investment mandate is clearly defined, investors typically do not have approval rights over individual deals. Instead, they rely on the fund manager’s expertise, track record, and governance framework.

Funds are usually structured as limited partnerships, with a general partner (GP) managing the fund and limited partners (LPs) providing capital. This model dominates institutional investing due to its scalability and diversification benefits.

Capital Deployment: Deal-Specific vs Pooled Strategy

One of the most important distinctions in the SPV vs fund structure debate is how capital is deployed.

In an SPV structure, capital is deployed deal by deal. Investors evaluate a specific opportunity, assess its risk-return profile, and commit capital only if it aligns with their objectives. This creates a high degree of intentionality and precision in portfolio construction.

In a fund structure, capital is pooled and deployed over time across multiple deals. While this provides diversification, it reduces investor control. Capital may be allocated to investments that individual LPs would not have chosen independently.

This difference makes SPVs particularly attractive for co-investments, thematic exposure, and opportunistic strategies, while funds remain well-suited for broad mandates and long-term capital deployment.

Transparency and Investor Control

Transparency is a major factor driving the growing adoption of SPV structures.

SPVs offer full deal-level transparency. Investors know exactly which asset they own, at what valuation capital was deployed, and how performance is evolving. Reporting is typically simpler and more focused, as it relates to a single investment.

Fund structures, while professionally managed, provide aggregated transparency. Investors receive portfolio-level reporting rather than granular insight into each decision. This is acceptable—and often preferred—by institutional investors seeking manager-driven diversification, but it can feel opaque to investors who want more visibility.

From a control perspective, SPVs allow investors to opt in or out of each opportunity. Funds require a higher level of trust and long-term commitment to the manager’s judgment.

Risk Profile and Diversification

Risk exposure differs significantly between SPVs and funds.

An SPV concentrates risk in a single asset or transaction. While this allows for targeted exposure and potentially higher returns, it also increases idiosyncratic risk. Poor performance cannot be offset by other assets within the same vehicle.

Funds, on the other hand, are inherently diversified. Losses in one investment may be balanced by gains in others. This diversification reduces volatility and downside risk but may also dilute upside from top-performing assets.

As a result, SPVs are often used by investors who already have diversified portfolios and are seeking incremental or opportunistic exposure, while funds appeal to those prioritizing risk smoothing and long-term allocation.

Fee Structures and Economics

The economic models of SPVs and funds differ in ways that materially impact investor returns.

Funds typically charge management fees (often around 2%) and carried interest (commonly 20%) on profits. These fees compensate managers for sourcing, executing, and managing investments over long periods.

SPVs generally have lower ongoing fees. There is usually no annual management fee, though sponsors may charge setup fees, administrative costs, and carried interest on profits. Because SPVs are deal-specific, fee structures are often more flexible and negotiable.

For investors, this means SPVs can be more cost-efficient for high-conviction opportunities, while funds justify their fees through diversification, infrastructure, and long-term stewardship.

Governance and Decision-Making

Governance frameworks also differ meaningfully between SPVs and funds.

In an SPV, governance is intentionally lightweight. A manager or sponsor executes the investment, while investors retain limited rights over major decisions such as amendments, early liquidation, or material changes to the deal.

Funds have more formal governance structures, including advisory committees, reporting standards, and regulatory oversight. This added complexity supports scale but reduces agility.

The simpler governance of SPVs makes them faster to execute and easier to customize, whereas funds prioritize stability, repeatability, and institutional standards.

Liquidity and Time Horizon

Liquidity is another key differentiator.

SPVs are generally illiquid until a defined exit event occurs. There is no expectation of interim liquidity, and secondary transfers may be restricted. Investors must be comfortable with holding the position until realization.

Funds also involve long lock-up periods, but they may generate interim liquidity through distributions from partial exits or cash-flowing assets. Additionally, institutional secondary markets for fund interests are more mature than those for SPVs.

Time horizon alignment is therefore critical. SPVs are best suited for investors with clear expectations around exit timing, while funds support longer, more flexible investment cycles.

Operational Complexity and Scalability

From an operational standpoint, funds are designed for scale. Once established, a fund can deploy capital across many deals without creating new legal entities each time.

SPVs, by contrast, require entity-level setup and administration for each deal. This includes legal formation, accounting, tax filings, and investor reporting. Historically, this limited SPVs to smaller or bespoke transactions.

However, modern fund administration and SPV platforms are rapidly reducing this friction, making SPVs scalable and repeatable without sacrificing efficiency.

When to Choose an SPV Structure

SPVs are particularly well-suited for:

Co-investments alongside lead funds

Venture capital syndicates

Real estate single-asset deals

Opportunistic or thematic strategies

Investors seeking maximum transparency and control

They are ideal when conviction is high and investors want targeted exposure without committing to a broader fund mandate.

When a Fund Structure Makes More Sense

Fund structures remain optimal for:

Broad diversification across assets

Long-term capital deployment

Institutional investors with large allocations

Strategies requiring continuous reinvestment

Manager-led portfolio construction

Funds excel when scale, diversification, and professional management outweigh the need for deal-level control.

SPV vs Fund Structure: A Strategic Choice

The debate between SPV vs fund structure is not about which is better in absolute terms. It is about strategic fit.

SPVs offer precision, transparency, and flexibility. Funds offer diversification, scale, and operational maturity. In practice, many sophisticated investors use both, allocating core capital to funds while deploying opportunistic capital through SPVs.

As private markets continue to evolve, hybrid approaches—where funds and SPVs coexist within the same investment ecosystem—are becoming increasingly common.

Final Thoughts

Understanding the differences between SPV and fund structures is essential for navigating modern private investing. Each structure serves a distinct purpose, and choosing the right one can significantly impact outcomes.

For investors, the key lies in aligning structure with objectives: risk tolerance, liquidity needs, conviction level, and desired control. For sponsors and managers, the challenge is offering the right vehicle for the right opportunity.

In today’s capital markets, flexibility is power—and mastering both SPV and fund structures is a competitive advantage.

If you want next, I can:

Addhyan Negi

Director of Marketing, Allocations

Start your next SPV

in 10 minutes

Start your next SPV in 10 minutes

Start your next SPV

in 10 minutes

Read related articles

Allocations secondary market is operated through Allocations Securities, LLC dba AllocationsX, member FINRA/SIPC. Check this firm on FINRA BrokerCheck. Allocations Securities, LLC is a wholly owned subsidiary of Allocations, Inc.

Copyright © Allocations Inc

Allocations secondary market is operated through Allocations Securities, LLC dba AllocationsX, member FINRA/SIPC. Check this firm on FINRA BrokerCheck. Allocations Securities, LLC is a wholly owned subsidiary of Allocations, Inc.

Copyright © Allocations Inc

Allocations secondary market is operated through Allocations Securities, LLC dba AllocationsX, member FINRA/SIPC. Check this firm on FINRA BrokerCheck. Allocations Securities, LLC is a wholly owned subsidiary of Allocations, Inc.

Copyright © Allocations Inc