SPVs

SPV in Venture Capital: How SPVs Are Used to Invest in Startups

Addhyan Negi

·

In modern venture capital, Special Purpose Vehicles, commonly known as SPVs, have become one of the most important structural tools for investing in startups. While they often operate quietly in the background, SPVs now power a large share of angel rounds, syndicates, scout programs, and even late-stage private transactions.

At their core, SPVs solve a simple but critical problem. Early-stage and growth companies want capital, but they do not want dozens or hundreds of small investors cluttering their cap table. Investors, on the other hand, want access to high-quality private deals without needing to commit to an entire fund or manage complex legal and tax work on their own. The SPV sits between these two needs and makes the transaction work smoothly for both sides.

What Is an SPV in Venture Capital?

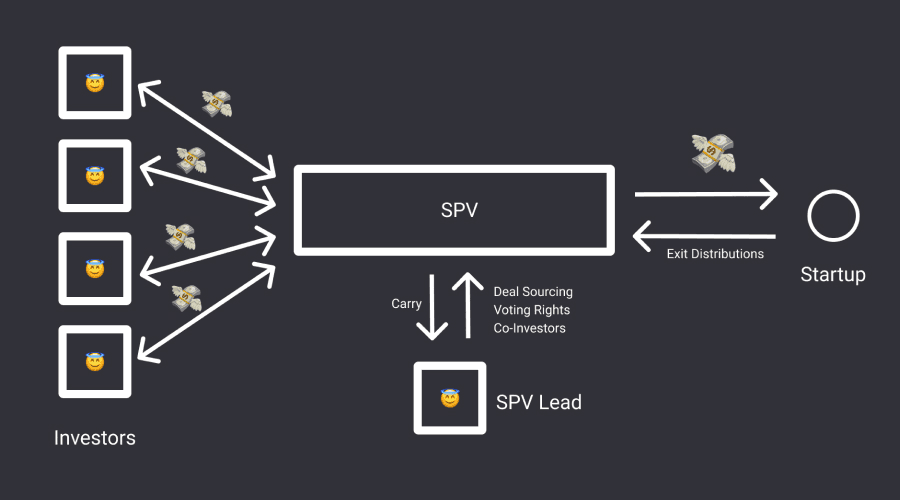

An SPV in venture capital is a single-purpose investment vehicle created to invest in one specific startup. Instead of each investor writing a check directly to the company, investors pool their capital into the SPV. The SPV then makes one consolidated investment into the startup and appears on the cap table as a single shareholder.

From the company’s perspective, this keeps ownership clean and governance simple. From the investor’s perspective, it provides access to deals that might otherwise be difficult or impossible to participate in individually. The SPV holds the shares, manages distributions, and handles ongoing administration until the investment exits.

This structure is now widely used across early-stage and late-stage venture deals, particularly as private markets have grown more competitive and globally distributed.

How SPVs Are Commonly Used in Venture Deals

SPVs show up across many parts of the venture ecosystem. Angel syndicates use SPVs to allow a lead investor to bring together dozens of smaller checks into a single allocation. Rolling funds and scout programs rely on SPVs to back individual companies without creating a new blind-pool fund for each strategy. Founder-led rounds often use SPVs when a startup wants to raise capital from a trusted network without opening the round to a broad set of direct investors.

SPVs are also increasingly common in late-stage secondary transactions. As companies stay private longer, employees and early investors look for liquidity before an IPO. SPVs allow buyers to purchase blocks of private shares while keeping the cap table streamlined and compliant.

High-profile companies such as SpaceX have frequently been accessed through SPV structures, allowing investors to participate in private rounds without the operational burden of direct ownership. Large hedge funds and family offices, including structures similar to those used by Citadel, also rely on SPVs to isolate exposure to specific deals or strategies.

SPV Fund vs SPV Company vs SPV LLC

Although the terminology varies, most venture SPVs fall into a small number of structural categories. An SPV fund typically refers to a pooled investment vehicle that brings together multiple investors for a single deal, often structured as a limited partnership or limited liability company. An SPV company is a broader term describing any standalone legal entity created for a specific transaction. In practice, most US-based venture SPVs are formed as SPV LLCs, which offer flexibility, pass-through taxation, and straightforward governance.

The phrase “SPV vehicle” is often used generically to describe any of these structures. Regardless of the label, the defining characteristic is that the entity exists for one investment and one investment only.

Bankruptcy-Remote SPVs and Risk Isolation

One of the most important but least understood features of an SPV is bankruptcy remoteness. A bankruptcy-remote SPV is structured so that its assets are legally separated from the sponsor or manager. If the sponsor encounters financial trouble, creditors cannot claim the assets held inside the SPV.

This separation is essential in venture capital, where investors expect their exposure to be limited strictly to the underlying startup. Bankruptcy remoteness is achieved through careful legal design, including independent governance provisions, narrowly defined operating purposes, ring-fenced bank accounts, and tightly drafted SPV agreements.

Beyond venture capital, bankruptcy-remote SPVs are also critical in credit strategies, securitization structures, and tokenized funds. As private markets become more complex and interconnected, this level of legal isolation is no longer optional. It is foundational.

SPV Accounts, Banking, and Capital Flow

Every SPV requires its own dedicated bank account. This is not just a best practice but a core compliance requirement. Investor funds must never be commingled with the sponsor’s operating accounts or with other vehicles. A clean banking setup ensures a clear audit trail, accurate reporting, and smooth distributions when liquidity events occur.

Modern SPV platforms now handle much of this complexity behind the scenes. They support bank account setup, capital calls, investor wiring, and distributions within a single system. This is where platforms like Allocations differentiate themselves by offering end-to-end SPV management rather than forcing managers to stitch together legal firms, banks, and spreadsheets.

How SPVs Are Formed

The formation of an SPV follows a relatively standard process. First, the sponsor selects a jurisdiction, most commonly Delaware for US deals or offshore jurisdictions such as the Cayman Islands for international structures. Next, the legal entity is formed as an LLC or limited partnership. The governing documents are drafted, including the operating or partnership agreement and investor subscription documents. A dedicated bank account is opened, investors are onboarded through KYC and AML checks, and capital is collected. Once the close is complete, the SPV deploys capital into the target startup.

What once took weeks or even months can now be completed in a matter of days with the right infrastructure in place.

SPV Agreements and Legal Governance

The SPV agreement is the legal backbone of the vehicle. It defines investor rights, economic terms, management fees, carried interest, voting mechanics, and how exits and distributions are handled. Depending on the structure, this may take the form of an LLC operating agreement or a limited partnership agreement, supplemented by subscription documents and side letters.

Well-drafted SPV agreements are critical not only for investor protection but also for operational efficiency. Clear terms reduce friction during exits and ensure that distributions are handled predictably.

SPV Loans and Credit Structures

In some cases, SPVs may also take on debt. An SPV loan allows the vehicle to borrow capital while keeping liability isolated from the sponsor. The assets held inside the SPV typically serve as collateral. This approach is used in venture debt, real estate SPVs, structured credit, and revenue-based financing strategies. As private credit markets expand, loan-enabled SPVs are becoming more common.

Ongoing SPV Management

SPV management does not end once the investment is made. Ongoing responsibilities include investor communications, tax filings such as K-1s, regulatory filings like Form D, distribution processing, and exit management. Audits may also be required depending on the structure and investor base.

Because of this ongoing workload, many investors and managers now prefer full-service SPV platforms over do-it-yourself approaches.

Comparing SPV Platforms

Traditional tools like Carta offer SPVs as an extension of their cap table services, but SPVs are not their core focus. Sydecar specializes in venture syndicates but remains largely VC-specific. Newer platforms such as Allocations aim to cover SPVs, funds, and emerging asset classes within a single infrastructure layer.

Modern SPV managers increasingly expect faster closes, support for international investors, flexibility across asset types, predictable pricing, and automation rather than manual paperwork.

Why SPVs Matter Going Forward

SPVs are no longer a niche tool used only by sophisticated funds. They have become the default building block of private market investing across venture capital, real estate, private credit, and digital assets. As ownership structures evolve and private markets continue to grow, SPVs will only become more central.

If you invest in private markets today, you are almost certainly using SPVs, whether directly or indirectly. Understanding how they work is no longer optional. It is foundational to modern investing.

Addhyan Negi

Director of Marketing, Allocations

Read related articles