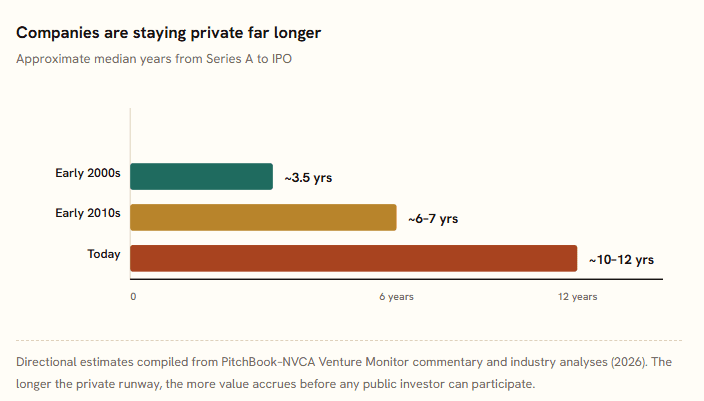

For most of the last century, the deal was simple: companies went public early, and ordinary investors rode the growth in their brokerage accounts. That deal has quietly expired. Today the average company takes roughly ten to twelve years to travel from its Series A to an IPO—up from three or four years in the early 2000s. By the time a marquee name finally lists, the era of explosive multiples is often already behind it, captured by venture funds, crossover investors, and a small circle of insiders.

That structural shift is the entire reason "pre-IPO investing" exists as a category. And it raises an awkward question for anyone serious about retirement: your IRA may be the largest pool of long-horizon capital you control, yet a conventional brokerage IRA can typically only buy public stocks, bonds, and funds—the very assets that have already given up their highest-growth years. A self-directed IRA (SDIRA) is the tool that closes that gap, letting retirement dollars buy private company shares, venture funds, and the special purpose vehicles (SPVs) that increasingly serve as the on-ramp to late-stage names.

This guide walks through the mechanics, the tax math, the landmines, the wider menu of pre-IPO assets, and—at the end—how a platform like Allocations actually stands up the SPV that holds a pre-IPO position. None of it is investment, legal, or tax advice; private markets are illiquid and high-risk, and the compliance rules are unforgiving. Treat what follows as a map, not a recommendation.

Part 01: What a self-directed IRA actually is

A self-directed IRA is not a special new account type invented by the IRS. It is an ordinary Traditional or Roth IRA held at a custodian that permits alternative assets. The tax treatment, contribution limits, and withdrawal rules are identical to any other IRA. The only thing that changes is the menu: instead of being walled into exchange-traded securities, you can direct the account into real estate, private debt, precious metals, crypto, private funds, and—our focus here—equity in private companies.

The catch is structural. Every IRA must be held by a regulated custodian; you cannot legally take personal custody of IRA assets. With a brokerage IRA, the broker is the custodian and simply restricts you to its product shelf. With an SDIRA, you hire a specialized custodian or trust company whose job is administrative, not advisory. As the major custodians are careful to state, they do not sell, endorse, or vet investments—they execute your written direction and handle the paperwork. The diligence, and the liability, sit with you.

Roth vs. Traditional: the choice that matters most for startups

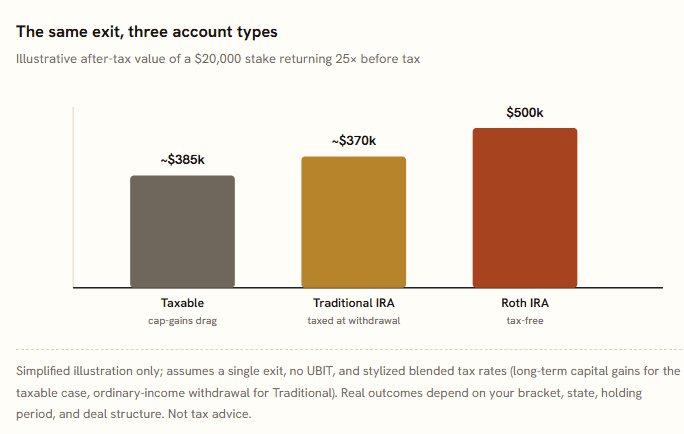

For a high-variance asset like a startup, the Roth-vs-Traditional decision is unusually consequential. A Traditional SDIRA is funded with pre-tax dollars and taxed on the way out. A Roth SDIRA is funded with after-tax dollars and—if rules are followed—every dollar of growth comes out tax-free. Now imagine a $20,000 stake that returns 25x when the company finally lists. In a Traditional account, the entire $500,000 is eventually taxed as ordinary income on withdrawal. In a Roth, that half-million is yours, untaxed, forever. This is precisely why the most aggressive private bets often belong in a Roth: the asymmetric upside is exactly what you most want to shelter.

The Peter Thiel point.

The reason a Roth holding private shares draws so much attention is the math above, taken to an extreme. Concentrating a moonshot inside a Roth converts a once-in-a-career outcome into a tax-free one. The same mechanics that make it powerful also make it ruthless if you trip a prohibited-transaction rule—more on that below.

Part 02: The contribution rules you are working within

Whatever you invest in, an IRA can only grow as fast as you can fund it. For 2026, the IRS raised the standard contribution limit to $7,500, with a $1,100 catch-up for those 50 and older (a combined $8,600). These caps are shared across all of your Traditional and Roth IRAs combined—not per account. Roth eligibility also phases out at higher incomes, while business-owner vehicles like the SEP IRA and Solo 401(k) allow dramatically larger annual contributions.

2026 contribution and eligibility figures (selected)

Account / parameter | 2025 | 2026 |

|---|---|---|

Traditional / Roth IRA limit (under 50) | $7,000 | $7,500 |

Catch-up contribution (50+) | $1,000 | $1,100 |

Roth full-contribution MAGI ceiling — single | — | < $153,000 |

Roth full-contribution MAGI ceiling — joint | — | < $242,000 |

SEP IRA / Solo 401(k) employer max (approx.) | — | up to $72,000 |

Total IRA contribution if 50+ (50+, combined) | $8,000 | $8,600 |

The practical implication for private investing is real: $7,500 a year will not, by itself, buy into a late-stage round with a six-figure minimum. Most serious SDIRA investors therefore fund the account by rolling over an old 401(k) or transferring an existing IRA—moving years of accumulated savings into a vehicle that can finally deploy them into private deals without triggering tax. A trustee-to-trustee transfer or direct rollover preserves the account's tax status; a clumsy 60-day rollover can blow it up.

Part 03 The tax case for holding startups in an IRA

Why bother with the friction at all? Because tax drag compounds. In a taxable account, every interim gain, distribution, and eventual exit is taxed, and those tax payments stop compounding for you. Inside an IRA, gains compound untouched until withdrawal (Traditional) or are never taxed at all (Roth). Over a multi-decade horizon—exactly the horizon a long-private startup demands—the difference is not marginal.

Simplified illustration only; assumes a single exit, no UBIT, and stylized blended tax rates (long-term capital gains for the taxable case, ordinary-income withdrawal for Traditional). Real outcomes depend on your bracket, state, holding period, and deal structure. Not tax advice.

The chart compresses a lot of nuance—a Traditional IRA's apparent shortfall partly reflects that ordinary-income rates can exceed long-term capital-gains rates—but the headline holds: the Roth keeps the whole exit. For an asset class defined by a few enormous winners and many zeros, sheltering the winners is most of the game.

Part 04 How the investment actually gets done

The operational path from "I have an IRA" to "my IRA owns a piece of a private company" is more procedural than most people expect, and the order matters.

Open an SDIRA with an alt-friendly custodian

Choose a custodian or trust company that explicitly supports private placements. Confirm they hold the asset titled in the IRA's name—e.g., "[Custodian] Custodian FBO [Your Name] IRA #..."

Fund it—usually by rollover or transfer

Roll over a former-employer 401(k) or transfer an existing IRA to reach a balance that can actually participate in a deal. New annual contributions can top it up.

Confirm eligibility for the specific deal

You do not need to be accredited to own an SDIRA, but most private placements require the investor—here, the IRA and its owner—to be accredited (roughly $1M net worth excluding home, or $200k income / $300k joint).

Direct the investment in writing

Submit an Investment Authorization Form plus the deal's subscription agreement and operating documents. The custodian funds it by wire from the IRA. With a checkbook-control structure you can wire directly from the IRA's own account.

Hold, value, and report

The asset lives inside the IRA. The sponsor supplies an annual fair-market valuation and a K-1; proceeds from any exit flow back into the IRA, never to you personally.

"Every dollar in, every dollar out, stays inside the IRA. The moment value leaks to you or your family before retirement, the structure breaks."

Part 05: The rules that can destroy the account

This is the section to read twice. The IRS does not restrict what an IRA can invest in nearly as much as it restricts who the IRA can transact with. Cross that line and the penalty is uniquely severe: the IRS can treat the entire IRA as distributed—not just the offending slice—triggering taxes and penalties on the whole balance and stripping its tax-advantaged status.

Disqualified persons

The IRA cannot transact with "disqualified persons." That circle includes you, your spouse, your parents and grandparents, your children and grandchildren and their spouses, and any entity 50% or more owned or controlled by that group. (Notably, siblings, aunts, uncles, and cousins generally fall outside the circle.) The IRA also cannot transact with anyone providing services to it—including advisors who are compensated on its assets.

Prohibited transactions

The forbidden moves fall into recognizable patterns: selling or buying an asset between the IRA and a disqualified person; lending to or borrowing from the IRA; personally guaranteeing a loan the IRA takes; or receiving any personal benefit from an IRA asset. For startup investing specifically, the trap is self-dealing: your IRA generally cannot invest in a company you already control, and you cannot draw a salary, take founder benefits, or otherwise enrich yourself from a company your IRA backs.

A bright line, not a judgment callThe IRS applies prohibited-transaction rules as a near-absolute prohibition. Intent does not save you on the automatic ("per se") violations—a transaction with a disqualified person is prohibited regardless of how fair the price was. The safest private bet is one where you are a purely passive investor in a third-party-controlled entity, with no board seat, no salary, and no side arrangement.

There is one famous piece of good news. Under the Swanson Tax Court precedent, an IRA can capitalize a brand-new company, because a company with no prior owners is not yet a disqualified person at the moment of initial funding. This logic underpins a great deal of legitimate startup formation funded through IRAs—but it is a narrow doorway, and the moment you start drawing benefits the analysis changes. Get a specialist involved before relying on it.

Part 06: UBIT and UDFI: the tax trap inside the tax shelter

Most investors assume an IRA never pays tax until withdrawal. Usually true—but two acronyms create exceptions that bite private investors in particular.

UBIT (Unrelated Business Income Tax) applies when your IRA earns income from an active business rather than passive investment. Passive income—dividends, interest, rent, long-term capital gains—is generally exempt. But if your IRA holds an interest in an operating business structured as a pass-through (an LLC or partnership taxed as such) and that business throws off active operating income, the IRA can owe UBIT—at trust tax rates, which climb to the top bracket at low income levels. UBIT generally kicks in once unrelated gross income exceeds $1,000 in a year, reported on Form 990-T.

UDFI (Unrelated Debt-Financed Income) applies when the IRA uses leverage. If a portion of an investment is bought with borrowed money, the share of profit attributable to that debt becomes taxable. Classic example: an IRA buys a property half in cash and half on a non-recourse loan—roughly half the net income is then UDFI.

Why this matters for startupsMost equity stakes in C-corporations—which is how the great majority of venture-backed startups are organized—do not generate UBIT, because the C-corp pays its own corporate tax before any value reaches shareholders. The exposure tends to appear when the IRA invests through a pass-through that itself conducts an active trade or business, or when leverage enters the picture. Structure-awareness is the whole defense here, and it is one reason the choice of investment vehicle is not a formality.

Part 07The wider menu: other pre-IPO assets

"Startups" is the headline, but a self-directed account can reach a whole spectrum of private-market exposure. Each carries a different risk, liquidity, and tax profile.

Direct primary shares

Buying equity or a convertible directly in a private company's funding round. Highest conviction, highest risk, longest hold.

Secondary shares

Buying existing shares from employees or early investors seeking liquidity—often the only way into a late-stage name. The fastest-growing corner of the market.

SAFEs & convertible notes

Early-stage instruments that convert to equity later. Simple to issue, but valuation and conversion terms drive the eventual outcome.

SPVs & syndicates

A pooled vehicle that invests in one deal, so many investors appear as a single line on the cap table. The dominant access route for individuals—covered in depth below.

Venture & PE funds

Diversified, professionally managed exposure across many companies. Higher minimums and fees; capital-call commitments rather than a single wire.

Pre-IPO / continuation funds

Vehicles aimed at late-stage names and GP-led continuation deals—an increasingly large share of how liquidity moves in private markets.

Private credit & venture debt

Lending to private companies for interest. Income-oriented—but watch the UBIT/UDFI analysis on active or leveraged structures.

Crypto, real estate & more

Tokens, rental and commercial property, tax liens, precious metals, and notes all live comfortably inside an SDIRA alongside private equity.

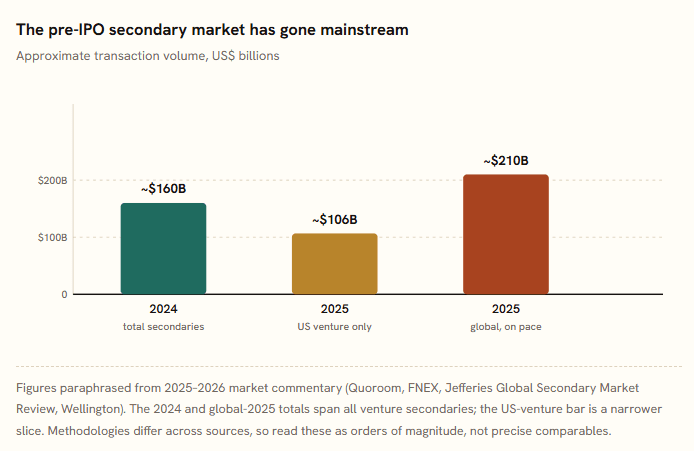

Among these, the secondary market deserves special attention, because it is where the pre-IPO opportunity has exploded. With companies staying private through their highest-growth years, employees and early backers accumulate valuable equity long before any IPO—and they want liquidity. That demand has built a deep, if uneven, marketplace.

ath that growth. First, the market is concentrated: a handful of elite names dominate volume, and analysts note that only a low-single-digit percentage of total unicorn value actually trades on the secondary market in any given year. Second, it is sequenced—when the biggest names finally list, they take much of the secondary liquidity with them, leaving a thinner second tier behind. Access is necessary; selection and pricing discipline are what separate good outcomes from bad ones.

Part 08: Why the SPV is the access vehicle

Here is the practical problem the SPV solves. A late-stage company guards its cap table jealously—every additional holder of record is administrative and legal overhead, and there are regulatory thresholds at stake. So it does not want fifty individual retirement accounts wiring in separately. It wants one line item.

A Special Purpose Vehicle (sometimes called a Single Purpose Vehicle) is a legal entity—typically a Delaware LLC—created for exactly one investment. Investors pool capital into the SPV; the SPV makes a single investment into the target company. The company sees one clean entry on its cap table; the investors get proportional economics, consolidated reporting, and a single K-1 flow. For an SDIRA holder, this is often the only realistic way in: your IRA subscribes to the SPV the same way it would any private placement, and the SPV does the rest.

SPVs also map neatly onto retirement compliance. Because a well-run SPV makes you a passive investor in a third-party-controlled vehicle—no board seat, no operating role, no salary—it sits squarely in the "safest" zone for prohibited-transaction purposes. And because most pre-IPO targets are C-corporations, the typical equity SPV does not generate UBIT. The structure is doing real work, not just paperwork.

Part 09: How Allocations sets up SPVs for pre-IPO companies

Historically, launching an SPV was a multi-week, multi-vendor slog: a lawyer to form the entity, a bank to open the account, a separate administrator for compliance and taxes, and a pile of email to chase signatures. Allocations collapses that into a single workflow built for speed and compliance—which is exactly what a time-sensitive secondary or pre-IPO allocation demands.

For a pre-IPO deal, the end-to-end flow looks like this:

Entity + banking, together. Allocations forms a standalone Delaware LLC and opens its integrated bank account as part of the same onboarding flow—eliminating the days or weeks usually lost coordinating a bank separately.

Digital investor onboarding. Subscription documents, e-signatures, and KYC/AML are handled in one place, including accreditation checks—so an SDIRA custodian can subscribe cleanly on the IRA's behalf.

Compliance, automated. Form D and blue-sky state filings are generated automatically, keeping the offering compliant without a separate securities-filing project.

Execute the investment. Capital flows from the SPV's account directly into the target—a primary round or a secondary purchase of existing pre-IPO shares.

Reporting & tax. The platform produces investor dashboards, a partnership return (Form 1065), and digital K-1s, then distributes proceeds back to investors—and back into each IRA—when the company exits, IPOs, or returns capital.

Built for the edge cases. Offshore structures for international investors and assets, crypto instruments, and blocker entities are all supported when a deal calls for them.

The commercial model is deliberately transparent: a Standard SPV carries a flat ~$9,950 setup fee covering formation, banking, investor onboarding (up to 35 investors), compliance, and tax prep across a multi-year term, with a Premium tier for larger or more complex raises and annual fund administration for multi-asset vehicles. Allocations takes no carry on these structures and charges no per-investor fee, with pricing published before you open an account. For an SDIRA investor or a syndicate lead assembling retirement capital into a pre-IPO name, that means the cost is knowable up front and the compliance scaffolding is handled by design.

Part 10: Before you commit: a sober checklist

Pre-IPO investing through a retirement account combines two of the most powerful tools in finance—tax-advantaged compounding and access to private growth—but it stacks their risks too. Keep these front of mind:

Illiquidity is the default. You may hold for a decade with no secondary market and no dividends. Money you might need before then does not belong here.

Valuations are stale and self-reported. Annual fair-market values are estimates, and last-round prices often diverge from what a share would actually fetch.

Concentration cuts both ways. A single name returning 25x is the dream; a single name going to zero inside your IRA is a permanent, un-deductible loss of retirement capital.

Compliance errors are catastrophic. A prohibited transaction can disqualify the entire account. Stay passive, keep family out, and use a knowledgeable custodian.

Get specialists involved. A custodian executes; it does not advise. Loop in a CPA who understands UBIT/UDFI and a securities attorney for anything non-standard.

The structural story is unlikely to reverse: companies have strong incentives to stay private, employees keep needing liquidity, and the infrastructure for compliant access keeps maturing. That makes a disciplined, well-structured pre-IPO allocation a legitimate part of a diversified alternative strategy for the right investor—and the self-directed IRA, paired with a clean SPV, is the vehicle that lets your retirement dollars participate in the growth that used to happen in public markets and now happens before the bell.

Important disclaimer: This article is for general educational purposes only and is not investment, legal, or tax advice. Allocations and the author are not your financial advisor, attorney, or CPA. Self-directed IRA rules, contribution limits, and securities regulations are complex and change; figures cited reflect publicly reported sources as of 2026 and may differ from your situation. Private investments are illiquid, speculative, and can lose all value. Consult qualified, licensed professionals about your own circumstances before acting.

SPVs

Read more

SPVs

Read more

SPVs

Read more

Company

Read more

SPVs

Read more

SPVs

Read more

Fund Manager

Read more

Fund Manager

Read more

Analytics

Read more

Analytics

Read more

Fund Manager

Read more

Fund Manager

Read more

Fund Manager

Read more

Company

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

Fund Manager

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

SPVs

Read more

Fund Manager

Read more

Fund Manager

Read more

Investor Spotlight

Read more

SPVs

Read more

Market Trends

Read more

Company

Read more

Analytics

Read more

Market Trends

Read more

Market Trends

Read more

Products

Read more

Fund Manager

Read more

Fund Manager

Read more

Fund Manager

Read more

Analytics

Read more

Market Trends

Read more

Fund Manager

Read more

Analytics

Read more

Analytics

Read more

Investor Spotlight

Read more

Analytics

Read more

Fund Manager

Read more